If you’re planning to move to Germany in 2026 whether for studies or work, there’s one requirement you absolutely can’t ignore. That is to prove that you have enough money to cover your expenses during your stay in Germany. And one of the best ways to do that is by opening a Blocked Account.

But here’s where it gets tricky choosing the right blocked account provider is not that easy. There have been cases in the past where providers froze the funds of international students and they couldn’t access a single euro for weeks. And trust me, the last thing you want is to get stuck in a foreign country without having access to your own money.

So in this article, I will explain everything you need to know about opening a Blocked Account in Germany. Main features, fees, reliability, and finally I’ll give you a detailed comparison of the top 3 blocked account providers so that you can decide which one’s right for you.

What Is a Blocked Account?

A Blocked Account, or Sperrkonto as it’s called in Germany, is a special type of bank account where you have to deposit a fixed amount of money initially. But here’s what makes it different from a current or savings account, you can’t just withdraw all the money at once. That’s why it’s called a “blocked” account.

Now, don’t worry, the money is still yours. It’s just that, you are only allowed to withdraw a fixed amount every month after you arrive in Germany.

Why? Because Germany is expensive, and the government doesn’t want you to overspend and end up broke halfway through your stay. And if it’s wintertime, trust me you don’t want to be sleeping on the streets.

Who Needs One?

Here’s the good news, you don’t need a blocked account for every type of visa. If you’re coming to Germany as a tourist, on a work visa, or on a Blue Card, you’re all good, no blocked account is needed. However, if you’re applying for an opportunity card or a job seeker visa, or if you want to come to Germany for studies, training, or even a language course then yes, you will need a blocked account.

How much do you need?

If you’re coming to Germany for studies, you’ll need to block €992 per month to cover your living expenses. That means for one full year, you must have €11,904 in your blocked account.

For other visa types, like the Opportunity Card, you are required to block about 10% more. So instead of €992/month, you’ll need to show €1,091/month, which comes to €13,092 per year.

This is as of 2025, but this number can change based on factors such as inflation, cost of living, and others. So always double-check before making any transfers. You can also deposit more than the minimum amount if your provider allows it, but I wouldn’t recommend it.

How to Choose?

There are a few important questions you need to ask before choosing a blocked account provider.

-

Where will your money actually be kept?

-

Is your money protected in case something goes wrong?

-

How easily can you access your funds?

Every provider in the market claims to be the fastest, safest, and most convenient. So you need to be careful here. Basically, there are two main types of blocked accounts:

Direct Bank model

In the direct bank model, the account is opened directly at a bank, either in Germany or another European country. Here the account is opened in your own name and your funds are protected under European deposit insurance laws. So this is generally considered the safest option.

Escrow model

In the Escrow model, your blocked account is not actually opened in your own name. Instead, it’s held by a trustee, inside an escrow account. The trustee could be a lawyer or a payment service provider and the connection between you and the trustee is defined by a separate legal contract. That means the money technically belongs to the Trustee, not you. Although this comes with some benefits, there is also some additional risk involved.

The best and safest approach

If you ask me, the best and safest approach is to open a blocked account in your own name with a bank that holds a full German banking license.

If you’re already in Germany, you can just walk into a local bank like Postbank or Sparkasse and open the account in person. But in most cases, when you need a blocked account, you’re applying from outside Germany. So it’s usually better to go through an intermediary. These are private companies that partner with licensed German or European banks to help you open your blocked account.

So before choosing any such account provider, check which bank they’re partnered with. Once you have the name of that bank, go to the official database of BaFin, which is Germany’s financial regulatory authority, and search for that bank. If they’re listed there, you’re good to go.

If you’re short on time and just need a quick answer, here are the three most popular and reliable providers in Germany:

-

Expatrio

-

Fintiba

-

Coracle

We’ll check each one in detail.

Fintiba

Fintiba was founded in 2016 and is actually the first digital blocked account provider in Germany. They’ve partnered with Sutor Bank, so you get a German IBAN and your money is fully protected under Germany’s deposit insurance.

It takes less than 10 minutes to open an account and you can do the whole process completely online. They also have a mobile app where you can track your account balance, see your monthly payouts, and contact support if needed. Plus, they also offer some additional services like health insurance and travel insurance.

What makes Fintiba unique is that you can deposit more than €11,904 if you want to. And it’s one of the few platforms that also supports underage students, with consent from the guardian.

The only drawback is that they don’t accept applications from U.S. tax residents right now, so if you fall under that category, you’ll need to look elsewhere. And when it comes to fees, there’s an initial account setup fee of €89, plus a monthly service fee of €4.90, which you have to pay upfront for the full 12 months.

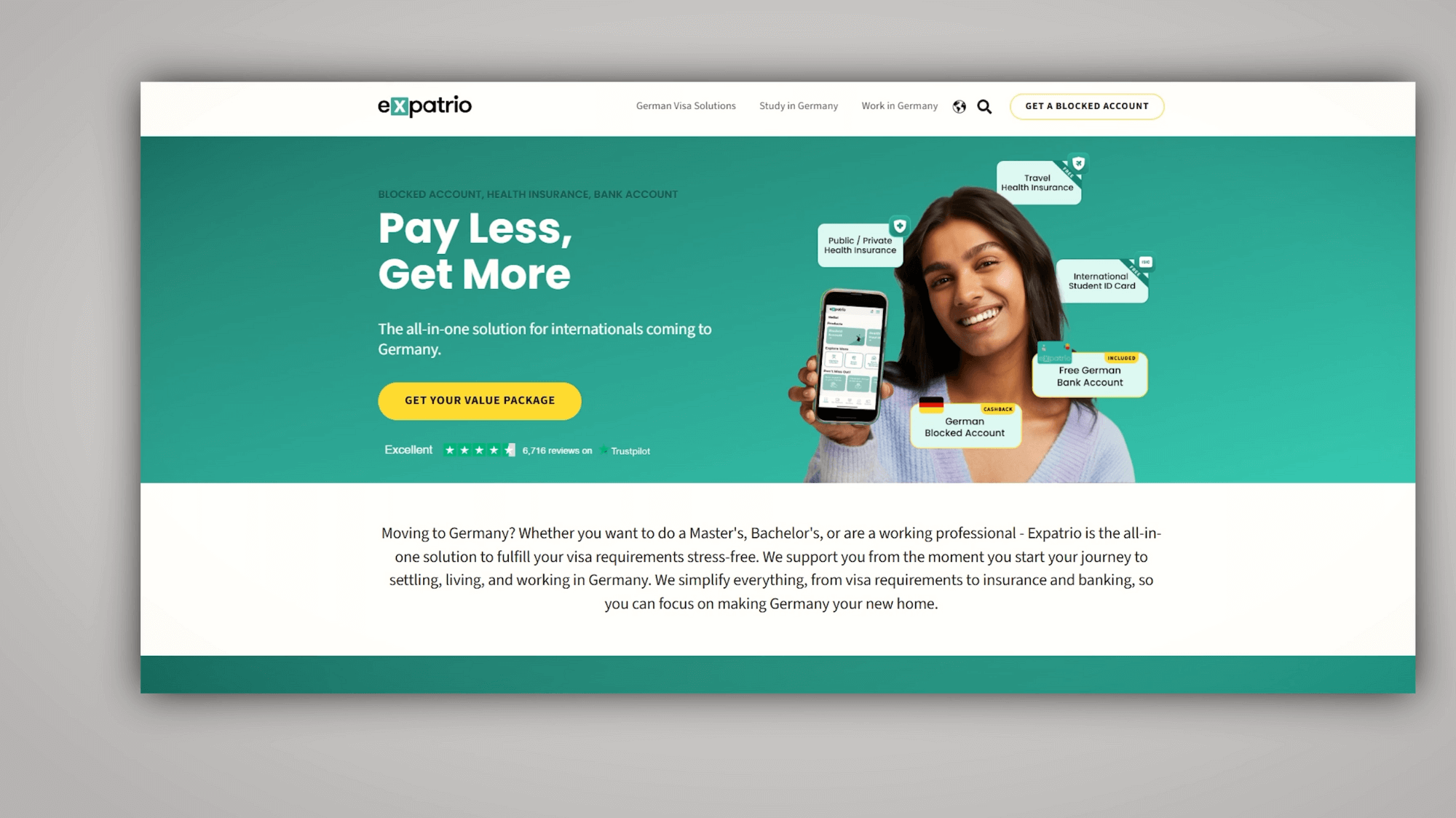

Expatrio

Expatrio was founded in 2017 and is one of the most student-friendly and popular blocked account providers in Germany. They partner with Aion Bank, which is based in Belgium, but they do have a subsidiary in Germany. So just like Fintiba, you get a German IBAN, and your money is protected under German deposit insurance. You can open the account in just a few minutes and everything is done online.

Expatrio is more of a one-stop shop for those who want to travel to Germany for studies or work. Along with a blocked account, you can also get health insurance, travel insurance, and even a current account. And if your visa gets denied, they also refund your fees, which is a huge plus. When we talk about the downsides: It’s not available for minors which honestly won’t matter for most of you. And you can’t deposit more than the recommended amount. When it comes to fees, there is a one-time setup fee of €69 and a monthly fee of €5 paid upfront for 12 months.

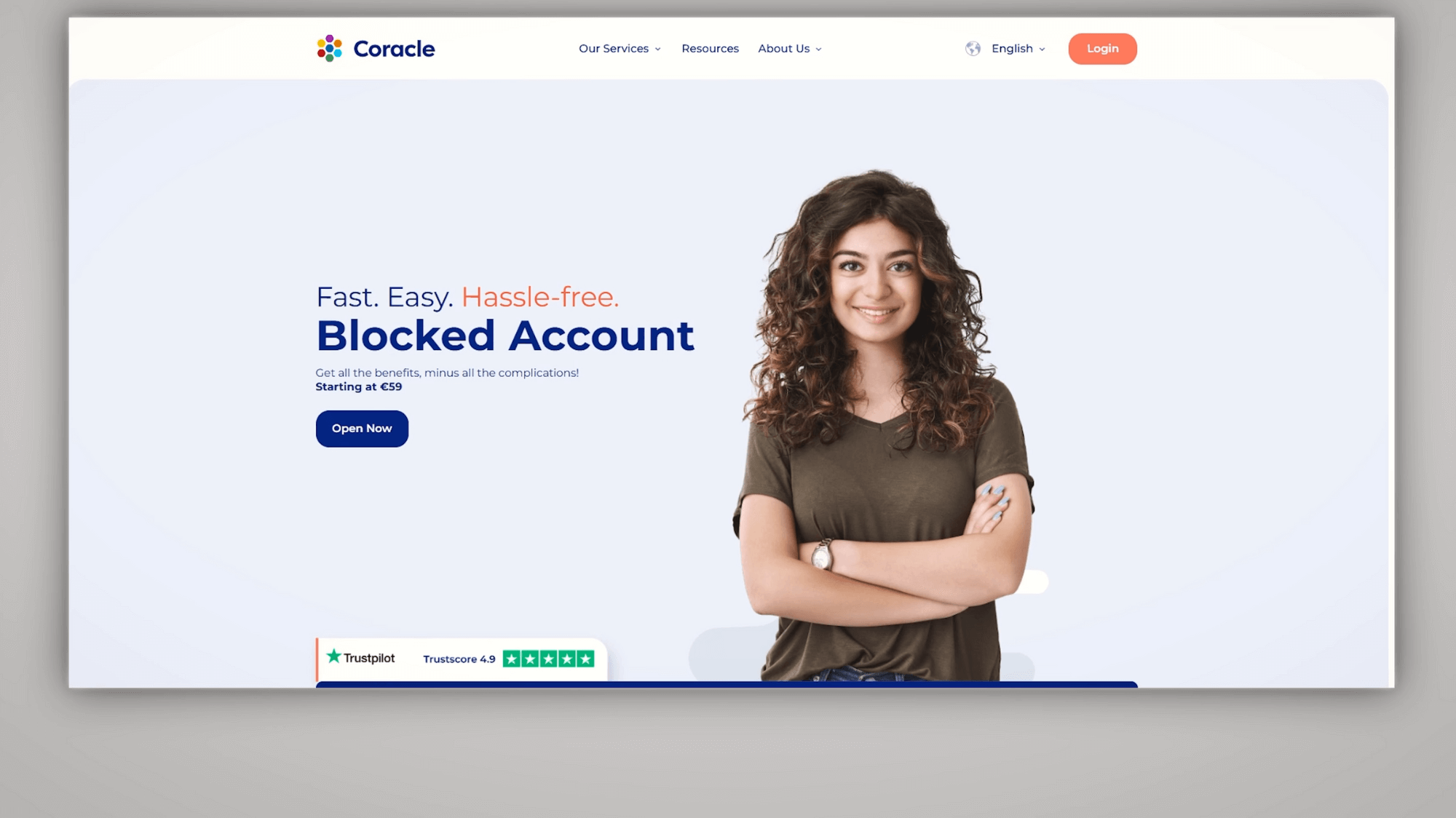

Coracle

Coracle started out in 2016 as a health insurance broker and later added the blocked account service. What sets Coracle apart from others is that they operate under an escrow model, meaning they work with a payment service platform called Lemonway instead of a traditional bank. So, your funds are held in a trust account rather than in your name at a German bank.

While Coracle is smaller than providers like Fintiba or Expatrio, it’s becoming more popular, mainly because of its zero monthly maintenance fees. You just have to pay a one-time setup fee of €99. And if you’re a student and choose their Prime package which also includes health and travel insurance, the total cost drops to just €59, making it one of the most budget-friendly options out there.

How to Open a Blocked Bank Account?

Before you go ahead and open a blocked account, the first and most important step is to check with your nearest German Embassy or Consulate, whether you actually need one for your specific visa type. If yes, find out the exact amount you need to deposit. Once that’s clear, choose from one of the providers according to your preferences, and it is accepted by the authorities.

Opening a blocked account normally involves 2 steps:

-

Fill out the application form where you will be asked a few details about yourself and your plans in Germany.

-

Upload your documents such as your passport, a photo, admission letter, and others.

Once you open your blocked account, the provider will send you the IBAN or the account number along with detailed instructions on how to make the transfer. Now you have two ways to send money to your blocked account. One, through an International Bank Transfer. This is the most secure option but takes more time and often comes with high fees. The best way to make the transfer is through a remittance service like Wise or Revolut. They’re usually faster, cheaper, and offer better exchange rates compared to traditional banks.

Once the transfer is done, it usually takes about 3 to 5 business days for the funds to show up in your account. After that, your provider will send you a blocking confirmation this is the document you have to submit with your visa application.

Before you can use your blocked account, you will have to activate it first. In most cases, you can do this through the digital platform of the provider except if you opened the account directly with a bank in Germany. In that case, you’ll most likely need to visit a branch in person to complete the activation. In both cases, you’ll generally need to provide supporting documents such as your passport with the entry stamp, your German residence permit, proof of city registration, your rental agreement, and proof of your current bank account in Germany.

Why do you need an extra current account?

This current account is where your monthly payouts from the blocked account will land, and it’s the one you’ll use for your day-to-day expenses: paying rent, buying groceries, your health insurance, and other similar expenses. Now, some providers like Expatrio or Fintiba offer a free current account, which is already connected to your blocked account. So it’s worth checking it out before you start your journey.

But keep in mind that access to your funds can sometimes be delayed. So better bring some extra money with you as cash to cover your initial expenses during the first few weeks.

Your blocked account typically stays open for the agreed duration, and if you don’t extend it, most providers will automatically close it after that period. But let’s say you finish your studies early or decide to return home, or if your visa gets rejected or you have to cancel your plans you can request to close the account earlier. In such cases, you will need to submit official proof and your personal bank account details where they should return the money.

No matter where your journey takes you, understanding how your blocked account works ensures you’re always prepared and in control. Auf Wiedersehen!

Disclaimer: The Content is for informational purposes only, you should not construe any such information or other material as legal or other advice. It is important to do your own analysis before making any decision.